In past renewal cycles, many condominium and homeowner associations saw relatively straightforward insurance renewals with incumbent carriers: updated applications, routine underwriting questions, and modest rate adjustments. Today, the landscape looks very different.

- Updated Prior Year Loss Runs Are Now a Standard Expectation

Just a few years ago, incumbent carriers often relied on the most recent loss run already on file and didn’t routinely request newer versions from prior policy years. Underwriters now want currently valued loss runs — across all prior policy terms — even when the broker hasn’t changed. This includes open claims with updated reserves, final paid amounts, and any adjustments made after the last reporting period. Accurate, up-to-date claims history helps carriers assess evolving exposures, trend patterns, and ongoing litigation risk more precisely.

- Greater Emphasis on Compliance With Prior Loss Recommendations

Underwriters are increasingly focused on whether associations are addressing mitigation recommendations from prior claims. For example:

- Roof repairs after repeated water intrusion claims

- Updated systems (roofs, HVAC, plumbing, electrical) when past life expectancy of current systems or current systems don’t conform with NFPA standards.

- Drainage improvements after recurring flooding

- Proof of testing for sprinkler systems and repairs for any items that failed.

Carriers want documented evidence that risk control suggestions are being implemented — not just acknowledged. Addressing recommended repairs and risk improvements proactively can significantly influence renewal terms and pricing.

- Enhanced Underwriting Scrutiny and Documentation

Insurers are asking for more comprehensive underwriting materials earlier in the renewal process, including:

- Loss histories for full prior terms

- Detailed responses to risk control questions

- Third-party inspection reports (e.g., roofs, boilers, structural)

- Compliance documentation for building codes or local ordinances

This trend reflects carriers’ desire to understand current risk profiles, not just historical ones.

- Market Competitiveness and Evolving Risk Appetite

The insurance market has seen shifts in capacity, carrier appetite, and pricing models across property and liability lines. These changes mean:

- Broader documentation requirements to access competitive markets

- More frequent requests for supplemental underwriting information

- Higher expectations for data accuracy and completeness

Renewals today require active management rather than passive submission.

What This Means for Property Managers and Boards

Insurance renewals now demand a partnership between property managers, boards, and brokers. Associations should expect to provide:

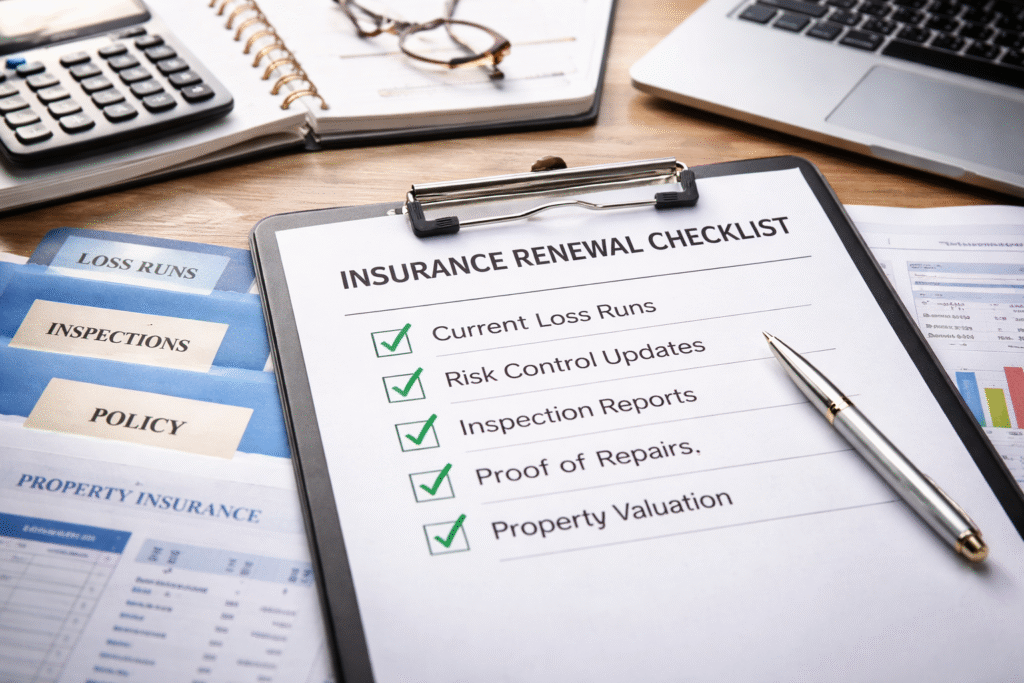

- Currently valued loss runs from current and prior carriers

- Evidence of risk control compliance

- Timely responses to underwriter requests

- Updated property valuations and exposure summaries

Engaging early in the process and providing accurate, complete information can lead to smoother renewals, stronger terms, and improved long-term risk outcomes.