Few challenges create more confusion — and more conflict — than insurance responsibility after a loss.

When multiple units are damaged, the first question is always:

“Is this the association’s responsibility or the unit owner’s?”

The answer depends on three critical factors:

- The condominium’s governing documents (declaration, bylaws, CC&Rs)

- State condominium statute

- How the master insurance policy is structured

Understanding how these pieces work together is essential for avoiding disputes, uncovered repairs, and unexpected financial exposure.

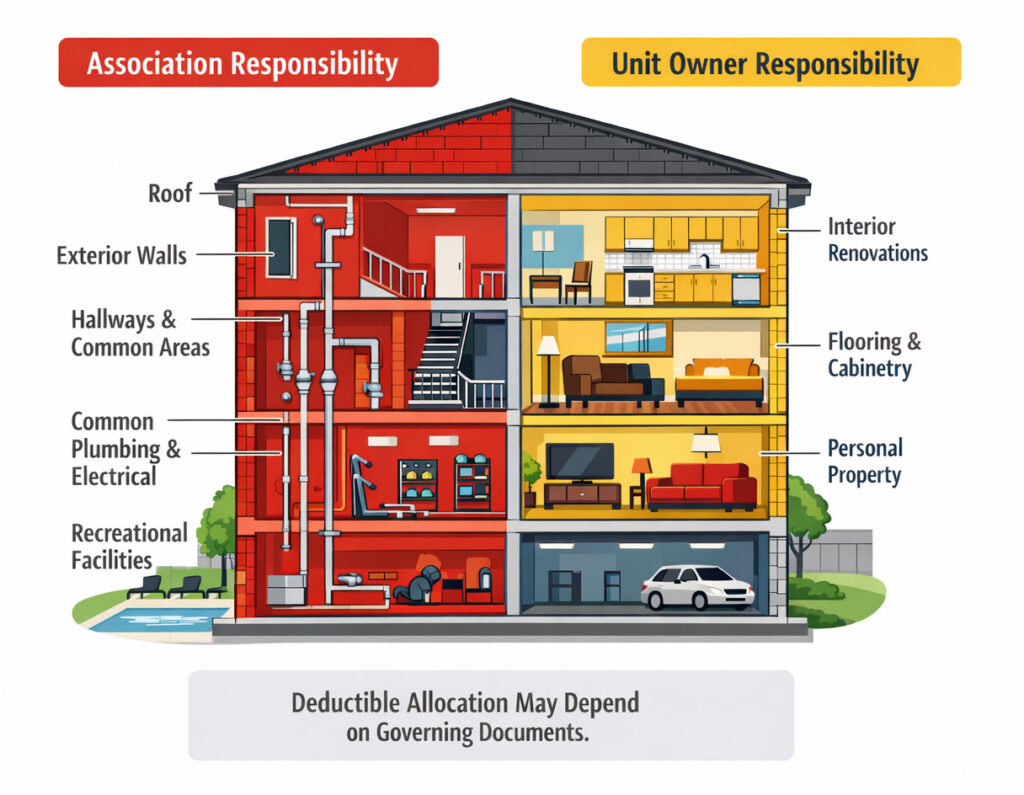

What the Master Policy Is Designed to Cover

The condominium master policy is intended to protect the property. However, the exact scope of coverage varies widely depending on how the documents define “unit” versus “common elements.”

Most master policies typically cover:

- Building Structure

This may include the shared building components such as:

- Roof systems

- Exterior walls

- Foundations

- Structural framing

- Plumbing, HVAC, and electrical infrastructure (if shared by multiple units)

Whether interior drywall or original finishes are included depends on how the documents define association responsibility.

- Common Areas

Typically covered common areas include:

- Clubhouses

- Fitness centers

- Pools

- Tennis courts and other similar recreational facilities

- Parking structures

- Association-Owned Property

This often includes items like:

- Maintenance equipment

- Furnishings in common areas

- Signage, fencing, and lighting

- General Liability for Common Areas

If someone is injured in a shared space, the association’s liability policy typically responds.

For example: A guest slips on an icy walkway outside the building entrance.

The Three Common Types of Master Policy Structures

Boards should understand which structure their policy follows:

Bare Walls

The association insures the building structure only. Unit owners insure nearly everything inside the unit, including drywall and fixtures.

Single Entity

The association covers the structure and original fixtures/finishes as initially constructed. This would include any upgraded options offered by the developer at the time of the first purchase.

All-In

The association covers the structure plus interior components, including improvements and upgrades.

Important: These labels may not appear in the policy itself. The governing documents ultimately control responsibility. The insurance carrier will review bylaws for each claim to determine the association responsibility.

What the Master Policy Typically Does Not Cover

Regardless of structure, master policies generally do not cover:

Unit Owner Personal Property

Furniture, electronics, clothing, and personal belongings are the responsibility of the unit owner’s HO-6 policy.

Upgrades and Betterments

When an owner upgrades original finishes, such as replacing carpet with hardwood flooring or installing custom cabinetry, responsibility for repair or replacement hinges on how the association’s documents define improvements and maintenance obligations.

This is one of the most common areas of dispute after a claim.

Additional Living Expenses

If a unit becomes uninhabitable, temporary housing costs are typically the unit owner’s responsibility under their HO-6 policy.

Interior Liability Within a Unit

If someone is injured inside a unit, the unit owner’s liability policy applies.

The Deductible Issue: A Growing Exposure for Associations

Many associations now carry large property deductibles — sometimes $10,000, $25,000, $50,000 or more — particularly for wind, hail, or water losses.

Occasionally, most often in the case of water damage claims, deductibles are applied per affected unit. Generally, this is applied to older associations with no documented plumbing updates or those that have had frequent or severe water damage claims.

Boards must understand:

- Who is responsible for the deductible when damage originates in a unit?

- Does the declaration clearly allow the association to charge back the deductible?

- Does state law limit how deductibles may be allocated?

If governing documents are unclear, the association may be forced to absorb the deductible — even when a loss begins in a specific unit.

If there are any questions about responsibility, it is always recommended to have an attorney review and offer their opinion based on legal requirements.

A Critical Governance Principle

Boards and managers should avoid giving owners direct coverage advice. Instead, encourage owners to:

- Review the association’s governing documents

- Consult their own insurance agent

- Confirm they carry adequate HO-6 and loss assessment coverage

This protects both the association and the manager from misrepresentation claims.

Final Thoughts

The master policy and the unit owner’s HO-6 policy are intended to work together — but they rarely align perfectly without careful oversight.

When documents, deductibles, and policies are misaligned, the result is often:

- Owner disputes

- Delayed repairs

- Unexpected assessments

- Financial strain on the association

Clarity before a loss is far less costly than conflict after one.

Need Help Reviewing Your Association’s Insurance Structure?

At Community Risk Advisors, we work with condominium boards and property managers to:

- Align governing documents with insurance programs

- Evaluate deductible exposure

- Clarify responsibility boundaries

- Strengthen claim response processes

If you would like a structured review of your master policy and insurance responsibilities, our team is here to help.