While governing documents often outline association responsibilities, state statutes add another layer of requirements that can significantly influence insurance decisions, financial planning, and the long-term protection of the property.

Understanding these state-based regulations is essential to keeping your community compliant and adequately insured. Here’s what board members and community managers should know.

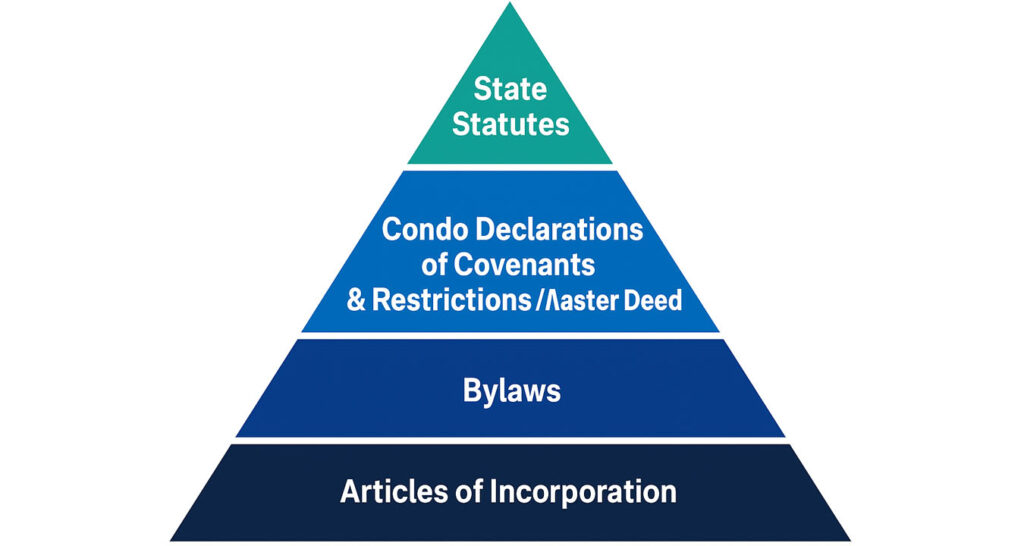

- State Statutes Have the Final Word

Every community association operates under a set of governing documents, but state condominium statutes ultimately supersede the association’s documents when it comes to minimum insurance requirements. These laws are designed to protect unit owners, lenders, and the financial stability of the association.

Most state statutes address key requirements such as:

- Minimum property insurance limits

- Coverage on building components (common elements vs. units)

- Responsibility for deductibles

- Requirements for general liability insurance

- Fidelity and crime coverage standards

- Certain types of mandated specialty coverage (e.g., flood, workers compensation, boiler & machinery)

Since these statutes vary widely by state, associations should work with insurance professionals who specifically understand community association regulations in their jurisdiction.

- Property Coverage Requirements: What Must Be Insured?

Nearly all states require the association to insure the common elements, such as:

- The building structure

- Roofs, exterior walls, foundations

- Shared mechanical systems

- Hallways, elevators, amenities, and common meeting rooms

Many states also define insurance responsibilities for portions of the units—for example, requiring coverage for drywall, ceilings, or original building materials while leaving improvements or betterments to the unit owner.

Understanding this breakdown ensures the association purchases adequate property coverage while avoiding unnecessary overlap with unit owner policies.

- Replacement Cost Requirements and Government-Backed Loans

Government-backed loans—especially Fannie Mae, Freddie Mac, and FHA—impose strict insurance guidelines to protect lenders and maintain financing eligibility for units within the community.

These loan programs typically require:

- Full replacement cost coverage for buildings and common elements

- No coinsurance penalties that could reduce claim payouts

- Adequate coverage to rebuild after a total loss

- Evidence of insurance compliance during loan underwriting

Associations that do not maintain proper replacements-cost property insurance may jeopardize owners’ ability to sell or refinance units. Ensuring alignment with these lending requirements is critical for maintaining property value and marketability.

- Understanding Liability Requirements

State laws usually mandate that associations carry commercial general liability insurance, often with minimum limits. Required areas of coverage typically include:

- Bodily injury claims

- Property damage to others

- Personal injury incidents

- Legal defense costs

Some states also require coverage for specific exposures such as:

- Directors & Officers Liability (D&O)

- Workers Compensation for employees (required regardless of whether full-time staff or temporary help is used)

- Umbrella or Excess Liability depending on community size or amenities

Liability coverage ensures the association stays financially protected when accidents, injuries, or governance-related disputes occur.

- Deductible Rules and Unit Owner Assessments

State statutes frequently outline:

- How property insurance deductibles must be allocated

- Whether the association can assess deductibles back to unit owners

- The maximum deductible amount permitted

- Requirements for notifying owners about rising deductibles

Some states allow associations to charge a deductible back to the owner of the damaged unit, while others require the deductible to be a common expense regardless of where the loss occurs.

Understanding your state’s rules prevents disputes with owners and ensures consistency in claims handling.

- Special State-Mandated Coverages

Depending on location and community-specific risk factors, state law may also require additional specialty policies, such as:

- Flood Insurance (especially in coastal or FEMA-mapped high-risk zones)

- Equipment Breakdown / Boiler & Machinery Insurance

- Environmental or pollution coverage for certain amenities

- Crime and fidelity coverage with minimum limits tied to reserve account balances

Failing to meet these minimums can create compliance issues and expose the association to significant uninsured risks.

- Regular Reviews Are Essential

Because state regulations evolve, community associations should:

- Review their insurance program annually

- Consult with insurance professionals who specialize in association risk

- Confirm that coverage meets both statutory and lender requirements

- Update policies as governing documents or amenities change

- Communicate insurance responsibilities clearly to unit owners

Staying proactive helps ensure the association remains fully protected and compliant.

Final Thoughts

State-based insurance regulations for community associations can be complex, but understanding them is vital for protecting the community, its property, and its financial stability. By working closely with an insurance agency that specializes in community associations and keeps current with evolving state laws, boards can confidently maintain a compliant and comprehensive insurance program.